Bank of Namibia Crypto Policy: Restrictions, Licensing, and the 2025 Reality

For years, if you asked anyone in Windhoek whether they could use Bitcoin to buy groceries, the answer was a hard no. The Bank of Namibia is the central bank of the Republic of Namibia, responsible for issuing currency and regulating the financial sector used to be famously skeptical, declaring in 2018 that it did not recognize cryptocurrencies as commodities or support their trading. That stance felt like a closed door for anyone trying to build a crypto business or simply pay for coffee with digital assets.

But things have changed. If you are looking at the current landscape in mid-2026, the door is still locked-but there is now a key. The regulatory environment has shifted from outright skepticism to a structured, albeit strict, framework. This isn't about wild-west speculation anymore; it's about compliance, licensing, and understanding exactly where the lines are drawn between legal tender and private virtual assets.

The Shift from Skepticism to Regulation

To understand where we are today, you have to look at how far the policy has come. In 2018, the central bank’s position was clear: no recognition, no support. Fast forward to 2022, and the tone softened slightly, acknowledging that merchants could accept Bitcoin if they chose to, even though it held no legal status. It was a small crack in the wall.

The real transformation happened in 2023. The National Assembly passed the Virtual Assets Act (Act No. 10 of 2023) legislation establishing the regulatory framework for virtual assets and service providers in Namibia. Alongside this, the Payment System Management Act was enacted. These two laws created the backbone of the current system. They didn’t make Bitcoin money in the eyes of the law-it remains without legal tender status-but they created a pathway for businesses to operate legally.

This shift matters because it moves the conversation from 'is it allowed?' to 'how do you get licensed?'. For entrepreneurs and investors, this clarity is invaluable. It means the risk of sudden bans is lower, provided you play by the new rules.

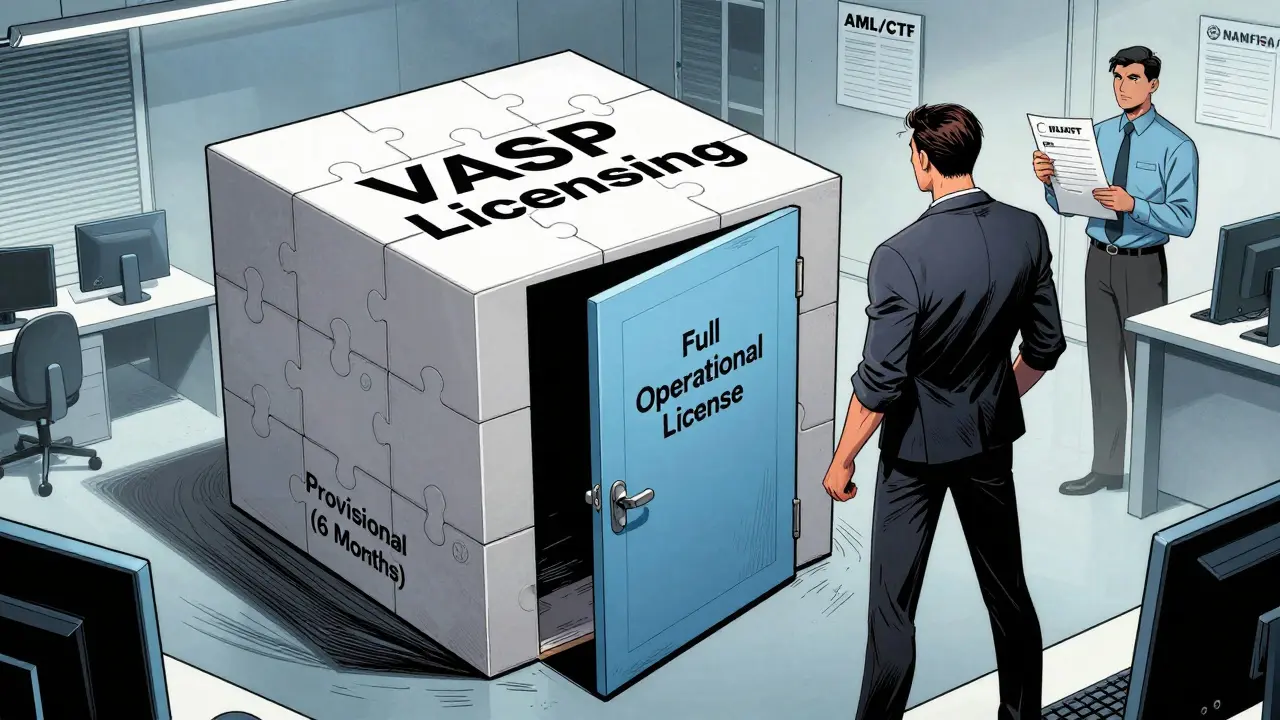

How the Licensing Framework Works

If you want to run a crypto exchange, offer custody services, or facilitate payments using virtual assets in Namibia, you cannot just open an office and start trading. You must become a Virtual Asset Service Provider (VASP) an entity authorized to provide services related to virtual assets, including exchange, transfer, and custody. The regulator here is not the Bank of Namibia directly for licensing, but rather the Namibia Financial Institutions Supervisory Authority (NAMFISA) the supervisory body responsible for overseeing financial institutions and implementing regulatory frameworks in Namibia, working in tandem with the central bank’s guidelines.

The process is designed to be cautious. It follows a two-step approach:

- Provisional Authorization: You apply and receive provisional authorization for six months. During this time, you are strictly forbidden from conducting any business or engaging with the public. You can hire staff, set up servers, and install software, but you cannot touch a single customer transaction.

- Full Operational License: After the six-month period, regulators inspect your setup. If you meet all conditions-including anti-money laundering (AML) and counter-terrorist financing (CTF) measures-you get full approval to operate.

This sandbox model is unique. Unlike some jurisdictions that let you launch under supervision, Namibia demands you prove you are ready before you even say hello to a client. It slows down revenue generation, but it significantly reduces the risk of fraud and systemic failure.

Key Restrictions and Compliance Rules

Even with a license, you aren't free to do whatever you want. The Bank of Namibia maintains tight controls to protect consumers and the financial system. Here are the non-negotiables:

- No Legal Tender Status: Cryptocurrencies are not money. Merchants can accept them, but they don't have to. Employees cannot be paid in crypto unless explicitly agreed upon, and taxes must generally be settled in Namibian Dollars (NAD).

- The Travel Rule: For transactions exceeding NAD 20,000 (approximately USD 1,000), VASPs must collect and share detailed information about both the sender and the receiver. This includes names, ID numbers, and account details. Privacy takes a backseat to security here.

- Ban on Foreign Exchanges: You cannot use crypto-exchanges that are not based in Namibia. This ensures that all significant activity happens within the regulated jurisdiction, making oversight possible.

- ICOs Are Off-Limits: The Bank explicitly warns against Initial Coin Offerings (ICOs). They view them as high-risk vehicles for fraud and manipulation. There is no support for the general public engaging in ICOs.

These rules might feel restrictive, especially if you are used to the decentralized ethos of crypto. But they reflect a pragmatic approach: allow innovation, but keep the risks contained.

Current Market Landscape: Who Is Licensed?

As of early 2025, the framework was actively being tested. The Bank of Namibia granted provisional authorizations to four entities: Finatic Technologies and United PayPoint for payment services, and Mindex Virtual Asset Exchange and Landifa Bitcoin Trade CC as VASPs.

However, the reality of compliance is tough. By mid-2025, several of these firms had requested extensions to their provisional periods. Landifa Bitcoin Trade CC sought an extension until July 2025, while Mindex Virtual Asset Exchange pushed its deadline to November 2025. This highlights a critical point: getting provisional approval is easy; meeting the rigorous operational standards is hard. The Bank conducts thorough due diligence, and if you aren't ready, you don't get to trade.

| Country | Regulatory Stance | Key Feature | Status (2025/2026) |

|---|---|---|---|

| Namibia | Moderately Progressive | Six-month sandbox before operation | Licensing active, strict compliance |

| Nigeria | Restrictive | Banks banned from facilitating crypto | High friction for users |

| South Africa | Advanced | VASP registration since 2022 | Mature market, established players |

| Botswana | Prohibitive | Complete ban on crypto trading | No legal avenue for trade |

| Ghana | Emerging | Comprehensive regulations planned | Implementation phase ongoing |

Namibia sits in the middle ground. It is more open than Botswana or Nigeria, but less mature than South Africa. This positioning makes it attractive for regional expansion, offering a safer harbor than unregulated markets but with higher entry barriers than laissez-faire jurisdictions.

The Future: rCBDC and Hybrid Ecosystems

While private crypto faces hurdles, the Bank of Namibia is simultaneously exploring its own digital currency. The concept of a Retail Central Bank Digital Currency (rCBDC) is under active consideration. Drivers for this include promoting financial inclusion, modernizing the payment system, and improving cross-border transactions.

This dual track-regulating private VASPs while potentially launching a state-backed digital dollar-suggests a hybrid future. Private cryptocurrencies will likely remain niche tools for specific use cases, heavily monitored and restricted. Meanwhile, the rCBDC could become the primary vehicle for digital payments, offering the speed of blockchain with the stability of fiat currency.

For businesses, this means watching two fronts. Keep your VASP license compliant for the private market, but prepare your infrastructure to integrate with a potential central bank digital currency when it launches. The technology may be similar, but the regulatory expectations will differ vastly.

Practical Advice for Stakeholders

If you are a merchant considering accepting crypto, remember that you are operating at your discretion. Ensure your accounting systems can handle the volatility and report gains correctly for tax purposes. Do not assume crypto is stable money.

If you are an entrepreneur, budget for the six-month silent period. You need enough capital to cover salaries, rent, and tech costs without any revenue. Rushing this phase will lead to rejection. Focus on building robust AML/CTF protocols from day one. The Travel Rule requirements are not suggestions; they are mandatory checks.

Avoid ICOs entirely. The Bank’s stance is clear, and attempting to raise funds through token sales without explicit regulatory backing is a fast track to legal trouble. Instead, focus on providing utility-based services within the licensed VASP framework.

Is cryptocurrency legal in Namibia?

Yes, but with conditions. While cryptocurrencies are not recognized as legal tender, the Virtual Assets Act of 2023 allows for the legal operation of Virtual Asset Service Providers (VASPs) who obtain proper licensing. Trading and usage are permitted within this regulated framework.

Can I use Bitcoin to pay for goods in Namibia?

Yes, if the merchant agrees. The Bank of Namibia states that acceptance of virtual assets for payment is at the discretion of the merchant and buyer. However, the merchant is not obligated to accept it, and the transaction does not carry the same legal weight as paying in Namibian Dollars.

Who regulates crypto businesses in Namibia?

The Namibia Financial Institutions Supervisory Authority (NAMFISA) handles the licensing of VASPs under the Virtual Assets Act. The Bank of Namibia sets the broader monetary policy and oversees the payment systems, ensuring alignment with national financial stability goals.

What is the "Travel Rule" in Namibian crypto regulation?

The Travel Rule requires VASPs to collect and share personal information of senders and receivers for transactions exceeding NAD 20,000. This includes names, identification numbers, and account details, aimed at preventing money laundering and terrorist financing.

Are Initial Coin Offerings (ICOs) allowed?

No. The Bank of Namibia explicitly discourages and does not support public engagement in ICOs due to high risks of fraud, manipulation, and misrepresentation. There is currently no regulatory pathway for launching ICOs in Namibia.

you guys really think this is progress? its just more red tape for people who actually want to build something real the whole point of crypto was to escape these archaic banking systems and now namibia is just creating a new layer of bureaucracy that costs millions in compliance fees while achieving nothing but control over the populace

the travel rule is basically admitting they dont trust their own citizens and want to monitor every single transaction like some dystopian surveillance state it makes zero sense from an economic standpoint because you are stifling innovation with fear instead of encouraging growth through freedom

while i understand the frustration with regulatory hurdles it is important to recognize that structure often provides the stability necessary for long-term viability without clear guidelines the entire sector remains vulnerable to sudden bans which have devastated markets in other countries before

the six-month sandbox period might seem restrictive initially but it allows companies to refine their security protocols and ensure they are ready for public interaction this cautious approach can actually protect consumers from scams and fraud which has been a major issue in unregulated spaces

perhaps we should view this not as a barrier but as a foundation for sustainable growth where trust is built through transparency rather than speculation alone

the distinction between legal tender and private virtual assets is fundamentally misunderstood by those advocating for unrestricted use cryptocurrencies lack the intrinsic value backing provided by sovereign states and thus cannot serve as reliable mediums of exchange in any formal economic context

namibias approach reflects a sophisticated understanding of monetary policy wherein innovation is permitted only within strict boundaries that preserve financial integrity the prohibition on foreign exchanges ensures that capital flows remain transparent and subject to domestic oversight which is essential for maintaining macroeconomic stability

i find it absolutely laughable that anyone would consider this framework 'progressive' when compared to jurisdictions that actually embrace decentralization you are essentially forcing entrepreneurs to jump through hoops designed by bureaucrats who barely understand blockchain technology let alone its potential

and don't get me started on the ban on icos what gives them the right to dictate how startups raise funds if your project is legitimate why should you need permission from a central bank to sell tokens this is pure gatekeeping disguised as regulation

honestly i feel like we are missing the bigger picture here yes there are rules but isn't that better than having no rules at all imagine if everyone could just launch an exchange tomorrow without any oversight chaos would ensue and ordinary people would lose their life savings to rug pulls

maybe the slowness is intentional maybe they want to make sure only serious players survive i know it feels restrictive but perhaps it's a safety net we haven't appreciated yet

look! on one hand, you have the excitement of entering a regulated market; on the other hand, you have the crushing reality of six months of silence with no revenue!! it's a bit of a paradox, isn't it?

but hey, if you're going to play the game, you gotta follow the rules, right?? the travel rule is annoying, sure, but it keeps the bad actors out, mostly. so, buckle up, put on your seatbelts, and prepare for a bumpy ride into the future of finance!

i think its interesting how they are trying to balance everything but honestly i am not sure if it will work out well for small businesses tho

the part about paying employees in crypto sounds cool but probably too risky given how volatile prices can be sometimes

from a fintech perspective, the VASP licensing model is actually quite robust, especially when compared to the fragmented approaches seen in neighboring countries, the integration of AML/CTF protocols directly into the provisional authorization phase suggests a high level of institutional maturity, albeit at the cost of agility for early-stage entrants

however, the exclusion of foreign exchanges creates a significant bottleneck for liquidity, potentially leading to higher spreads and reduced trading volumes, which could stifle market depth in the short term

finally some sense in africa 🇳🇦 most countries are just letting wild west crypto happen and getting scammed left and right namibia is doing it right by protecting its citizens first 😎

if you cant handle a little regulation then maybe you dont deserve to trade anyway keep it safe and local 💪

everyone seems to forget that south africa has had vasp registration since 2022 and still struggles with enforcement so why do we expect namibia to magically solve all problems just because they wrote a law

the table comparison is misleading because it ignores the actual operational capacity of namfisa which is limited compared to larger economies

as someone who has lived in both windhoek and johannesburg i can see the appeal of namibias cautious approach it feels safer knowing there is a regulator watching over things even if it means slower growth

but i worry about the rcbdc becoming too dominant and crowding out private innovations which are often more creative and user friendly

it is truly inspiring to see such deliberate steps towards financial inclusion through digital means the emphasis on education and compliance shows a commitment to responsible development which benefits society as a whole

we should applaud these efforts rather than criticize them for being slow because speed without direction leads to disaster

why bother with all this complexity when you can just use cash or regular banks crypto is just a bubble waiting to burst again and namibia is wasting resources chasing a ghost

people should focus on real jobs instead of gambling on digital coins

the notion that this framework represents 'clarity' is utterly absurd, it is merely a labyrinth of contradictions designed to confuse and deter, the ban on foreign exchanges is particularly egregious, as it isolates the market from global liquidity pools, thereby depressing asset values and limiting investor choice

furthermore, the insistence on collecting personal data for transactions over nad 20,000 is a blatant violation of privacy rights under the guise of security, which sets a dangerous precedent for civil liberties

i really appreciate the detailed breakdown of the licensing process, it helps demystify what can be a very intimidating landscape for newcomers, understanding that there is a structured path forward gives me hope that legitimate businesses can thrive here

it's heartening to see regulators taking a proactive stance rather than a reactive one, which often leads to harsher penalties later on

oh my gosh, who has time for all this paperwork? 😩 i mean, seriously, six months of doing nothing but setting up servers? that sounds like a nightmare for anyone trying to make a living

but hey, if you love filling out forms, go ahead, i'll be over here enjoying my anonymity on decentralized platforms 👋💅

do not be fooled by the benevolent facade of namfisa, this is merely the first step in a grand conspiracy to monitor every movement of wealth within the nation, the travel rule is not about security, it is about control, ensuring that no dissenting voices can fund themselves outside the state's purview

they claim it prevents terrorism, but we know it prevents freedom, watch closely as they tighten the screws further with the rcbdc, turning us all into nodes in their digital panopticon

great summary of the current situation! 👍 for anyone looking to enter the market, i highly recommend starting with a thorough review of the virtual assets act, specifically section 12 regarding aml requirements

also, dont underestimate the importance of building relationships with local legal counsel early on, it can save you countless headaches during the provisional authorization phase 🚀

i agree with the sentiment that clarity is key, however, i wonder if the six-month silent period might discourage smaller startups who lack the capital to sustain operations without revenue

perhaps a tiered licensing system could allow micro-vasps to operate with lower limits initially, fostering grassroots innovation while maintaining oversight

actually, i think the ban on foreign exchanges is a brilliant move, it forces competition among local providers, driving down fees and improving service quality over time

plus, it ensures that customer support is available in local languages and time zones, which is a huge plus for everyday users

let us discuss the broader implications for regional integration, if namibia succeeds in creating a stable regulatory environment, it could become a hub for cross-border payments within southern africa

this would require collaboration with neighbors like botswana and ghana, despite their differing stances, to create interoperable frameworks

the assertion that cryptocurrencies hold no legal status is technically accurate yet practically irrelevant insofar as market participants voluntarily engage in transactions denominated in such assets, the critical factor lies not in statutory recognition but in contractual enforceability and tax compliance mechanisms

thus, the focus should shift from debating legal tender status to establishing robust judicial precedents for dispute resolution involving virtual assets

typical government overreach trying to control money supply while pretending to support innovation meanwhile the average citizen gets screwed with high fees and limited options

its just another way to keep the poor poor and the rich richer through monopoly power

sarcasm aside, the hybrid ecosystem idea is fascinating, imagine using rcbdc for daily expenses and private crypto for speculative investments, it could offer the best of both worlds, stability and opportunity

though i doubt the transition will be smooth, given the historical resistance to change in financial sectors

i appreciate the nuanced view presented here, it highlights the complexities involved in regulating emerging technologies without stifling their potential

hopefully, policymakers will continue to engage with industry stakeholders to refine these regulations as needed